WEDNESDAY, JUNE 21, 2017

Calculate Your Life Insurance Needs

How valuable are you to your family? Are you the bread winner, do you share equal responsibility with your spouse, or do you take care of the children and house 120 hours a week. The need for Life Insurance exist in all.

Calculators

How much life insurance do I need?

To help answer questions in the risk survey. The average funeral is $7,000 to 10,000. Final expense of closing our an estate cost 3-5% of total assets.

Term Life Quote

I you need help with the life quote please call or email me at David@jordanagency.com

Prices and coverages ARE NOT guaranteed until after health exam.

FRIDAY, JUNE 16, 2017

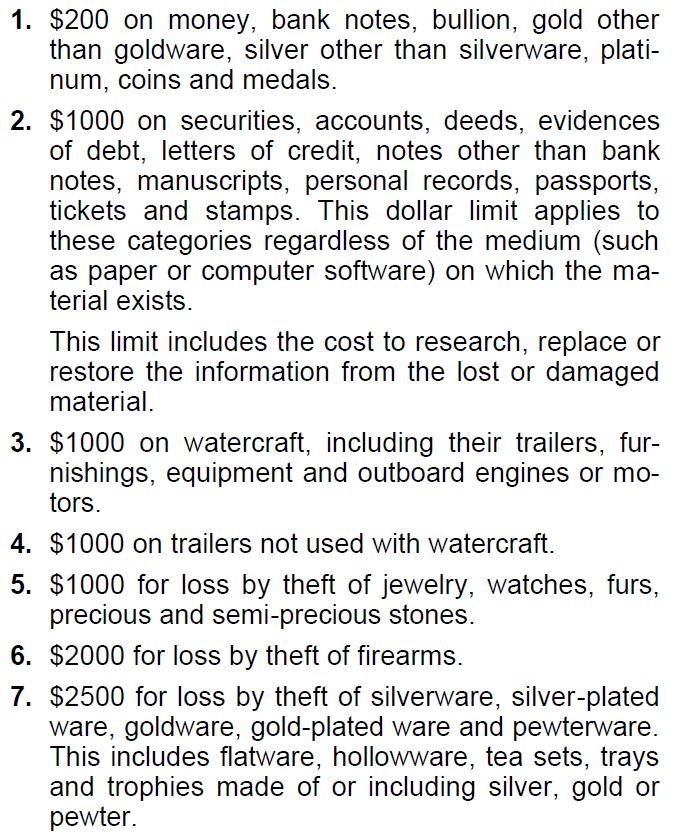

Homeowners, Condominium, and Renters insurance policies have Contents coverage built in to each policy. The best way I can communicate contents coverage is if you turned your house upside down what fell would be deemed contents. Something very important that many clients don’t know about their content coverage is the limited coverage items that are truly valuable to them.

Jewelry Coverage

Finding out that you have had your cherished heirlooms stolen can be devastating news, and buying new pieces won’t truly replace what you have lost, but if you do have valuable jewelry it is advisable that you take a look what you have and then sit down with your insurance agent. For jewelry theft, expect a maximum homeowners payout of $1,000 (total aggregate not per item), and half that amount under a renters policy.

Here is a more complete list of coverage

Most of the coverages listed above can be endorsed to an appropriate level for you and your family on a new or existing policy.

Here is a Link to more information on Homeowners coverage or to request a homeowners quote.

THURSDAY, JUNE 15, 2017

Many clients ask how their insurance rates are generated. Insurance companies produce a formula with the 4 factors below and present the proposal to The Department of Insurance. The DOI looks at the statistics and either Accepts or Declines the proposal to increase or decrease rates.

Recently many auto carries have gotten their increase rate approved at a state average of 10%. The justification for this change is directly correlated to increased claim occurrences resulting from distracted driving accidents, and even though you personally may turn off your phone while operating a vehicle. Though insurance premiums are determined by your driving record, an increase to the base rate effects every demographic a little differently. As you will see 2 of the 4 factors you can’t control.

These are 4 important factors that are taken into account; Zip Code, Age, Claims history, and vehicle model/year:

- Zip Code - Where you live will determine much of the base rate applied to your account. How dense the population is or the population’s average age. Even the percentage of insured to not insured drivers in your area. Statistically drivers will be involved in

more accidents in a big city than in a small town. Insurance companies are able to counter act that by adjust premium to cover losses within a community, so a customer in North Florida is not feeling the effects of 4 of July traffic jams on I-4. more accidents in a big city than in a small town. Insurance companies are able to counter act that by adjust premium to cover losses within a community, so a customer in North Florida is not feeling the effects of 4 of July traffic jams on I-4.

- Age - Each company has their own rating beliefs when it comes to age. Some companies believe that driving ability improves at a faster rate. So they are cheaper on younger drivers. While others will rate older drivers better believing driving ability decreases at a slower rate. The severity of accidents affect higher rates on drivers as well. Accidents with young drivers tend to happen on average, at higher speeds causing the damage done to be much higher. While older drivers have accidents at a slower speed, but the personal injury in those accidents are much greater because the body can’t handle the force nor does the body recover at the same rate.

- Claims History - Most people understand if you’ve had claims and tickets your chance of having more claims is higher so your premium is adjusted to take that into account.

This is not levied against you forever though. Most events fall off the report after 3 years to 5 years.

- Vehicle Model/Year - When you look at an Auto policy cost is broken into separate coverages; Liability (people suing you), Personal injury, and collision/comprehensive (repairing your vehicle). The larger the vehicle the more damage it does so Liability increases. The smaller vehicle the less it protects your body so personal injury increases. Thanks to new technology your family can be safer with all the automated sensors but you don't save money. The increase in repair cost drive the cost to a net equal, simple repair on a bumper that would normally cost $1200 dollars now cost $6000 to replace.

If you have seen an increase in your insurance rates and would like to have your policy reviewed, feel free to call our office at 386.362.4724 or email us and an insurance agent will reply promptly.

WEDNESDAY, MAY 10, 2017

Differences Between AHCA and ACA.

1. No More Mandate to Purchase or Provide Coverage

The plan eliminates the individual and employer mandate penalties. This means people will no longer be fined for lack of insurance, and large companies do not have to pay if they do not offer insurance to their employees. However, the plan allows for insurance companies to charge if a person was uninsured for 63 continuous days during the previous year.

2. Medicaid Expansion

The ACA’s plan to grow Medicaid is being halted. New enrollment freezes in 2020.

3. Abortion Funding Is Restricted

Any facility that offers abortions will not receive federal funding, including Planned Parenthood. Individuals that receive a plan with a subsidy cannot have abortion coverage.

4. Taxes on the Health Care Law Would Be Repealed

The plan removes the taxes on prescription drugs, over-the-counter medications, health-insurance premiums, and medical devices that the ACA used to pay for their plan.

5. Essential Health Benefits

The AHCA eliminates the requirement for Essential Health Benefits. The AHCA allows limited policies that are only in case of major illness or injury.

6. HSA and FSA

HSA contribution limits would be increased to match high deductible health plan out of pocket limits, and spouses would be able to make catch-up contributions to the same HSA.

The AHCA would change several current rules that apply to health Flexible Spending Accounts (FSAs) and Heath Savings Accounts (HSAs).

HSA and health FSA could be used for over the counter medications. Currently, HSA and health FSA funds cannot be used for over the counter medications without a prescription.

The next step is for the legislation to be moved on to the Senate, where it will likely face serious challenges. Senator Rand Paul has proposed S.R 222 that is different from the AHCA. The CBO has yet to score this bill with the amendments.

FRIDAY, MAY 5, 2017

Current Similarities between

AHCA and ACA.

1. Pre-Existing Conditions Will Still Be Covered

Under the Affordable Care Act, insurance companies are required to cover pre-existing conditions. This is still the case under the AHCA, but the creation of High Risk Pools, funded with $8 billion dollars was an added amendment to the AHCA. Pools provide coverage if you have been locked out of the individual insurance market because of a pre-existing condition, and are subsidized by a state government. The premium is up to twice as much as individual coverage. Individuals who have a lapse in coverage of more than 63 days will be required to pay a 30 percent premium surcharge for 12 months when coverage is purchased.

2. Adult and College Aged Children Up To Age 26 Can Still Remain on Parents’ Health Plan

People who are under 26 years old can stay on their parents’ health insurance plan under both the ACA and the AHCA.

3. No Lifetime Cap

Before the Affordable Care Act many plans set a lifetime limit, a maximum dollar amount that were covered in the plan. The ACA prohibited this, and it is still prohibited under the AHCA.

4. Tax Credits

The AHCA includes an advanced tax credit, but it is based on age and family size rather than income level.

|

Blog Archive

|